Investment Committee 01/06/2020

Modern | Dynamic | Honest

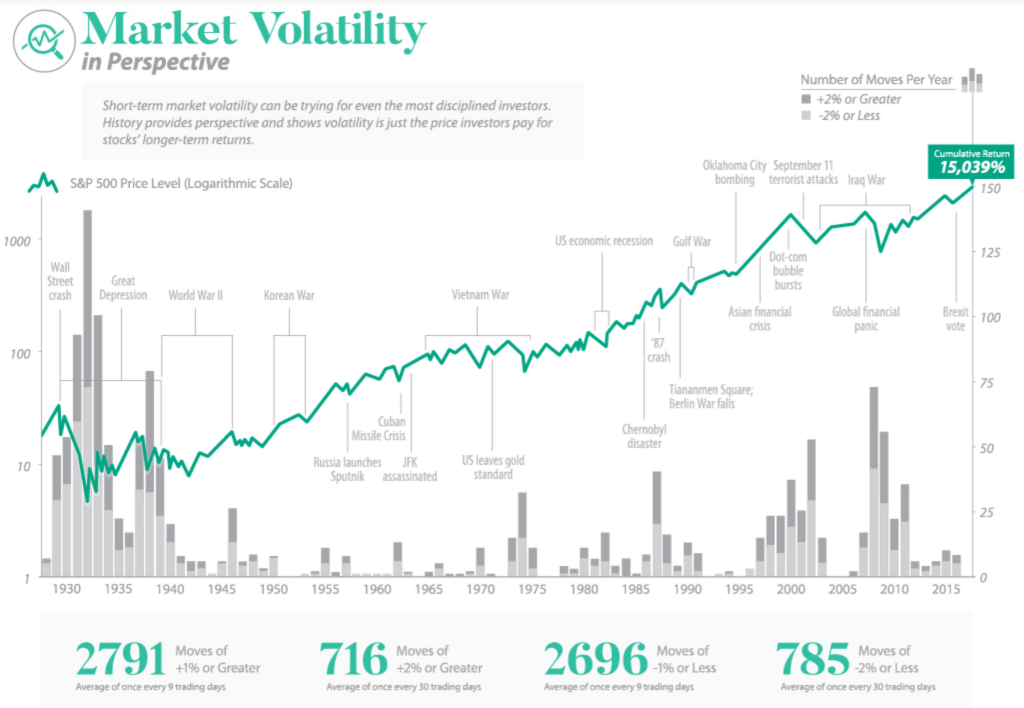

It has been an unprecedented quarter, none of our team have ever experienced anything like it which includes the fallout from the credit crisis, the dot com bubble, a few wars and the 1987 crash. That said, we think this chart of volatility, market moves and returns from the Visual Capitalist helps put things into perspective:

On reflection, the confidence that investors rediscovered during April’s equity market recovery continued through May despite a stream of negative company news (and there was a lot), and sadly we saw a rising Covid-19 death toll with further evidence that the global economy will suffer the deepest recession in living memory. Financial markets are of the opinion that the worst of the virus-related disruption is already behind us in terms of overall economic activity, and there is some truth in this, as countries around the world relax lockdown restrictions. However, we would continue to urge caution and would expect further volatility ahead.

This positive sentiment has largely been fueled by the unprecedented scale of policy support offered by central banks across the globe, as well as levels of fiscal loosening that one might usually associate with wartime. The markets’ rally has consequently begun to broaden out to embrace more economically sensitive companies, as opposed to the initial recovery which featured mainly “all weather” defensive companies and those that benefited directly from the dislocation. Even so, there remain myriad uncertainties which have the potential to create future obstacles.

Uppermost is the progression of the virus, with the threat of a “second wave” of infections not to be ignored. This could either be the result of increased social interaction or driven by the (yet unproven) seasonality of the virus. However, we remain hopeful that something will work:

Looking ahead we believe equities are yet to bounce back to any level considered ‘greed’ and we should keep faith with equities outside of the US. We expect the dollar to fade as elections draw near in the US and with the continued challenges they face. We continue to be underweight in US equities compared to our peers, we believe this market has been overpriced mostly due to the Tech stocks.

Our longstanding decision to avoid direct property again appears to be paying off, Covid-19 has highlighted how technology and home working can work without impacting productivity, as such we expect to see further long term pressures on this asset class, in particular commercial property which lacks liquidity in times of crisis.

We believe our preference towards active management will continue to be the most appropriate strategy over the long term, despite active managers being faced with increased pressure on their charges where performance has lagged against cheaper passive alternatives. Going forwards we can see the value active managers can add in picking the right stocks and not just following the market. Across the board our portfolios have sheltered our clients from much of the drawdown risk when compared to the market.

This article is for information purposes only – should not be perceived as financial advice. We recommend you should always speak to a financial adviser before making any investment decisions.

Please note past performance is not reliable indicator to future returns.

Your investment may fall as well as rise and you may not get back what you put in.