Investment Committee 01/09/2020

Modern | Dynamic | Honest

The last 3 months from a stock market view in the UK has been fairly flat at time of writing, we’ve not seen much movement in the FTSE100 which represents the 100 largest traded companies in the UK, which is now worth less than iPhone maker Apple alone – simply staggering. In the US on the other hand, their stock markets are now at all-time highs and are positive for 2020, another staggering observation.

Chris Bailey our head Economist has labelled this quarter as the market versus the economy versus the virus, it’s not hard to understand why…

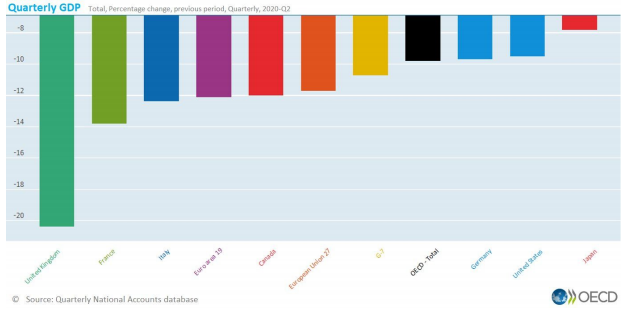

We all knew the Q2 economic contractions were going to be very bad, the chart below demonstrates some of the better-known regions that suffered from Covid-19:

Across the globe different asset classes have responded differently, equities have reacted positively and government fixed interest markets quite differently, this is no doubt linked to the large amount of government debt that has been accumulated in trying to combat and counter the consequences of the Coronavirus.

This response has made us view different regions with different attitudes, for example we feel the US is very overpriced with tech and medical stocks in particular starting to look like a potential bubble. For this reason, we continue to have an underweight position in this area and have a bias towards value rather than growth, which feels out of hand, especially as the Coronavirus rages on in the US which has started to weaken the US Dollar. This is good news for global equities and emerging markets (something we’ve expected to happen for some time).

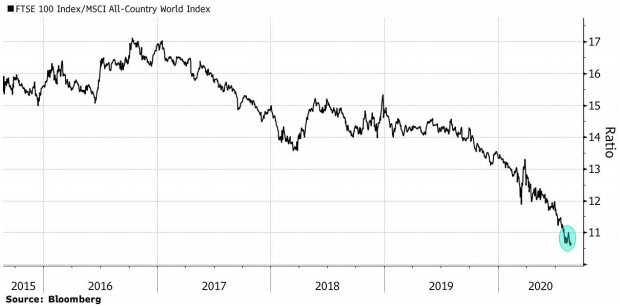

In contrast, the UK and Europe feels oversold and offers long term growth potential, this is illustrated below and shows how UK stocks are trading near their lowest level relative to global peers; this could potentially offer real value for investors.

However, clearly the UK and Europe are not out of the woods yet and we are constantly reminded with travel corridors opening and closing on a regular basis, resulting in worrying news for travelers and those who depend on travel for work. Let us also not forget we still have Brexit agreements ongoing which need to be concluded by December, however with everything that is going on let’s not rule out a further extension to trade talks…

An interesting side note from Chris Bailey, speaking recently to institutional investors in the US they have started to consider and move money out of the US into global equities, which will be good news for share prices across many regions including the UK and EU.

Apart from Coronavirus and Brexit, we also have the US elections to consider, the main worry here would be if Trump is re-elected and he continues to fuel a trade war with China, which could be made worse by the US response to China following the Covid-19 outbreak.

We should also consider inflation, despite low interest rates the fear of inflation is real and should not be ignored. Holding inflation proofing bonds still feels like a sensible move along with allocation towards alternative asset classes, which provide some hedge and diversification away from just relying on equities.

We believe our preference towards active management will continue to be the most appropriate strategy over the long term, despite active managers being faced with increased pressure on their charges where performance has lagged against cheaper passive alternatives. Going forwards we can see the value active managers can add in picking the right stocks and not just following the market.

Finally, Chris Bailey leaves us with this big thematic thought:

There is always something to worry about otherwise Economics would not be the ‘dismal science’ or have such a fine array of jokes targeted at it. But there are always options. If you want to build resilience then you must look within and focus on efficiency, simplicity and innovation. You may not be able to cost cut, print (money) or tax your way to success but a continuous cycle of improvement and innovation underpinned by the right incentives can go a long way. It is certainly not headline-grabbing nor individually particularly revolutionary, but whilst we wait for a Covid-19 vaccine it is certainly the best course of action for a consumer, household, employee or employer alike, as policymakers grapple in a world of economic trade-offs. As for equity investors, focus in on companies and countries that understand this best, especially if the market does not give them due credit today.

This article is for information purposes only – should not be perceived as financial advice. We recommend you should always speak to a financial adviser before making any investment decisions.

Please note past performance is not reliable indicator to future returns.

Your investment may fall as well as rise and you may not get back what you put in.